Get in touch with our career team!

We are passionate, intelligent and forward-looking team of financial advisers with an eye on the markets and the future.

Published on

LATEST POST

Articles, events, industry best practices, and news.

3 min read

Published on

Money in our Supplementary Retirement Scheme (SRS) account is meant to be kept till the statutory retirement age and certainly not meant to be served as liquid cash. Withdrawing it before the statutory retirement age may mean negating all the tax savings we enjoyed at onset when we contributed to our SRS account. This is because the amount withdrawn will be subjected to a 5% penalty and added to our current year assessable income by IRAS.

Since we are not going to withdraw it or use it anytime soon, and keeping the money sitting in SRS account yields only a pathetic 0.05% annually, it is a no brainer for us to get our money in SRS to work harder for better returns by investing in other approved instrument.

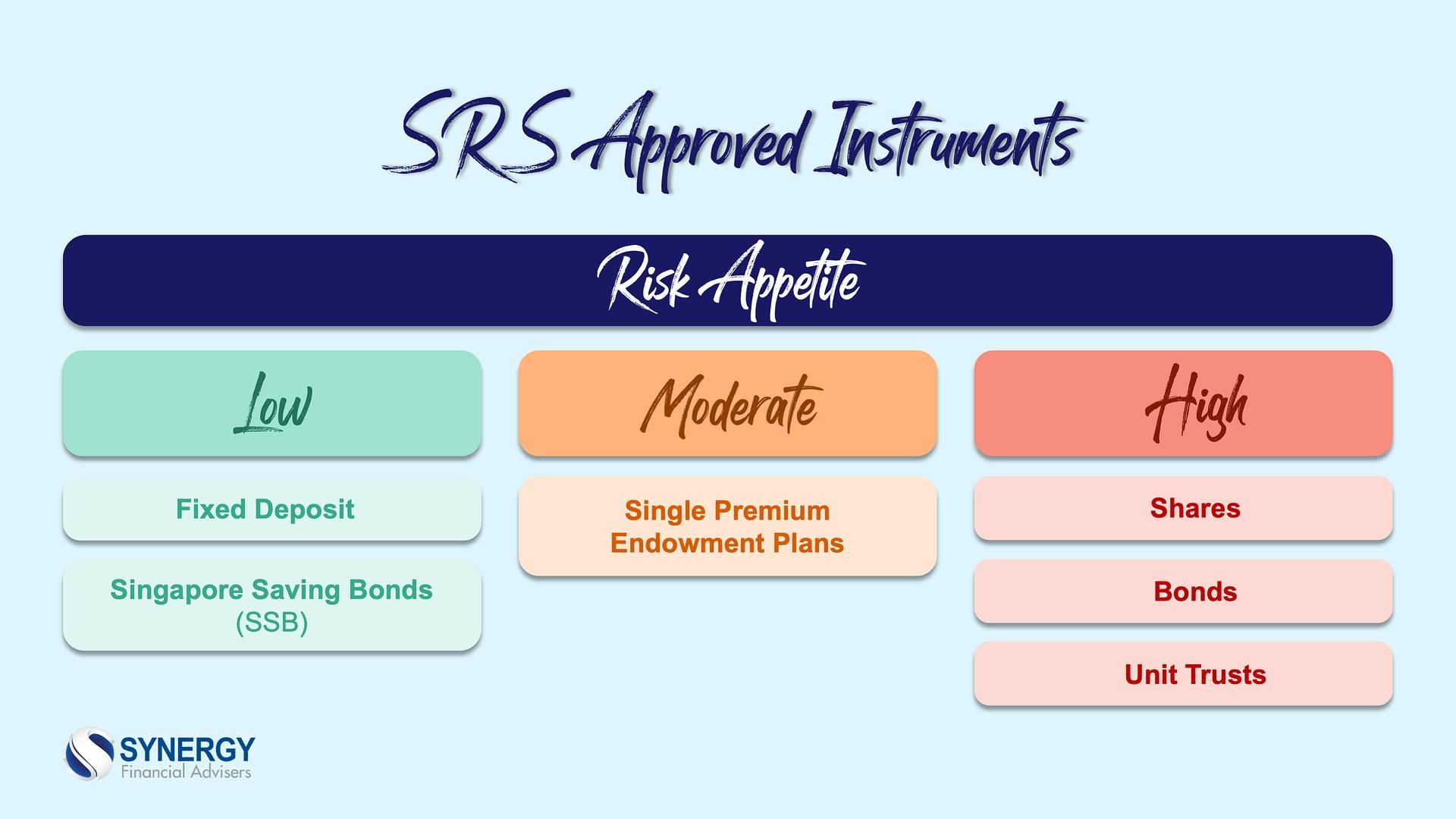

Among the list of approved instrument, the least risky option will be Fixed Deposit (FD) or Singapore Saving Bonds (SSB) which currently pays around 0.5% to 1%. Still pathetic right? Although they are almost risk-free, we still face reinvestment risk when we renew them, especially when global interest rates are trending towards zero in the foreseeable future. Ideally, it will be great if these instrument will mature at the statutory retirement age but FD and SSB typically only have maturity period of up to 18 months and 10 years, respectively.

If our appetite for risk is high enough, then buying Shares, Bonds or Unit Trusts are good ways to improve returns. If risking our funds in SRS is not what we will consider, buying Single Premium Endowment Plan will be the next best available choice to get better returns than just leaving it in the SRS account.

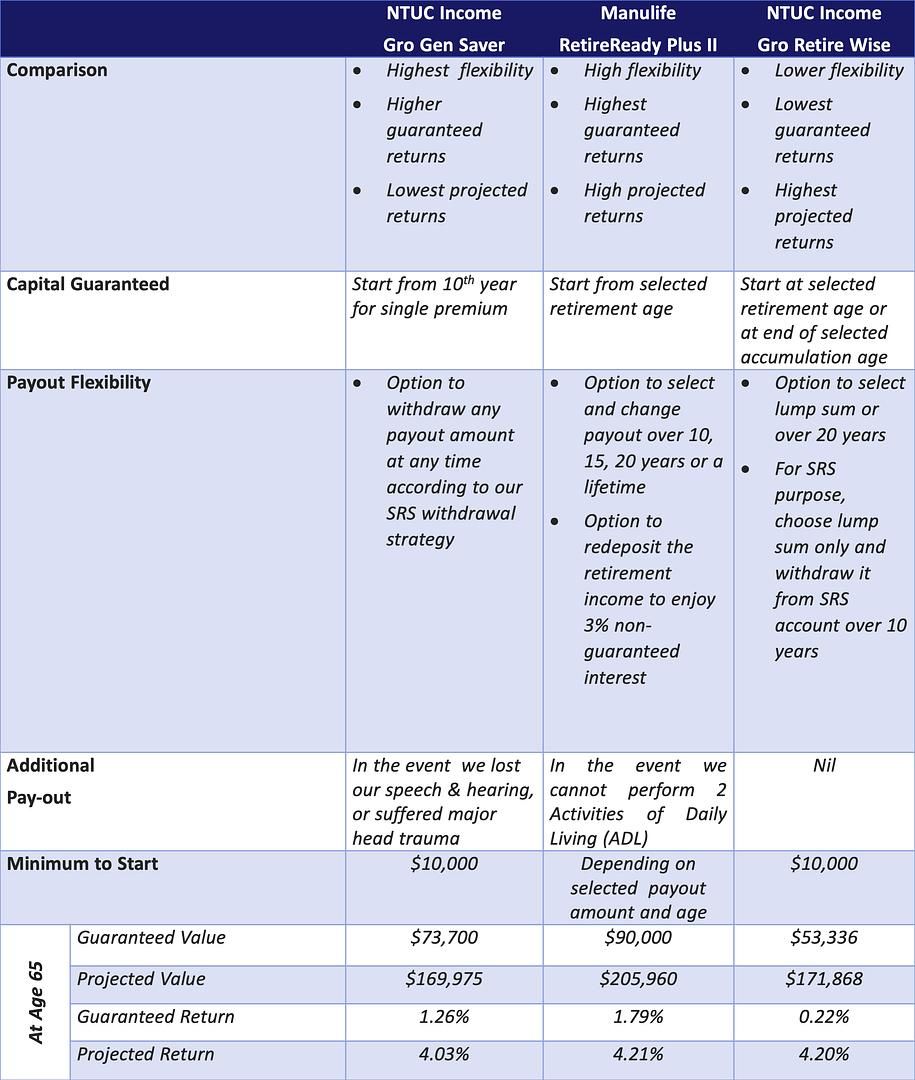

In the market, there are many approved Single Premium Endowment Plans that have comparable returns and benefits, but offer quite different withdrawal options and features. Our product advisory team have analysed and compared 3 endowment plans in the market we think offer the best value and payout features for our funds in SRS.

See the summary below for the comparison which is based on the benefit illustrations of the respective product for a 35-years-old non-smoker male investing about $50,000 of his SRS funds and receiving payout from age 65.

As we can see, each of the product illustrated has its own pros and cons. While NTUC Income’s Gro Retire Wise offer the highest projected returns at age 65, it give the lowest guaranteed return, and it provide the least flexibility in terms of payout options and additional benefits. On the other hand, Manulife’s RetireReady Plus II offer a decent overall return and highest guaranteed return while still providing some form of payout flexibility.

Which product to choose will depend on whether we prefer to minimise our tax payable when we retired, and on our specific retirement objectives. If we are not sure about our specific retirement objectives yet, then having flexibility in withdrawal options will be important.

For more information, you can speak with one of us or discover Synergy.

You may view our disclaimer on https://synergy.com.sg/disclaimer-general-advice.

LATEST POST

Articles, events, industry best practices, and news.