Get in touch with our career team!

We are passionate, intelligent and forward-looking team of financial advisers with an eye on the markets and the future.

Published on

LATEST POST

Articles, events, industry best practices, and news.

8 min read

Published on

In Singapore, the insurance landscape can be a bewildering place. The Monetary Authority of Singapore (MAS) mandates that direct purchase insurance (DPI) be offered by the life insurers. This new channel allows consumers the option of purchasing insurance directly from insurers, without going through a middleman. But what exactly is direct purchase insurance? How does it differ from the traditional way of buying insurance? Is it better or worse for consumers?

Direct Purchase Insurance (DPI) is a class of broadly standardised products offering term insurance or whole life insurance, and which include Total and Permanent Disability (TPD) coverage. DPI also provides Critical Illness (CI) coverage if you opt for it. DPI is identified by the prefix “DIRECT” in the product name.

You can buy DPI from the customer service centre, or website if available, of life insurance companies. DPI is sold without financial advice. Simplified for consumers to directly buy from life insurance companies, DPI is a basic life insurance and with option to add critical illness coverage, allowing for a straightforward purchasing process without a financial adviser. That's because it's marketed as a basic product that covers the life insurance and critical illness insurance that you fundamentally need to have for yourself and your dependents. In the event of your passing or if you are diagnosed with a critical illness such as major cancer, a heart attack, or a stroke, your insurance will pay out.

DPI Term Plan: The term insurance offered by DPI is available only for 5 and 20 year terms, or coverage up to age 65. This leaves clients with a kind of insurance that may not particularly tailored to their needs. In contrast, financial advisers can provide term insurance solutions that are fully customised to fit specific requirements.

DPI Whole Life Plan: DPI whole life plans lack the multiplier effect on the sum assured during an insured's economically active years compared to a whole life plan through advisory. Moreover, the products through advisory seem to provide better premium payment options. Options range from a mere 5 years to 25 years, with the upshot being that there is a lot of room for flexible financial planning while DPI only have option of premium paying till age 70 or age 85.

Limited Critical Illness Coverage: DPI is designed to protect against 30 serious illnesses, a far cry from the more than 37 covered by most policies purchased from financial advisers. And while some protection policies also cover "early" critical illnesses, those valuable benefits are completely absent from the DPI.

As DPI policies are sold without financial advice, they don't come with the sort of commissions that drive up your costs. Instead, you may pay premiums lower than those for comparable life insurance products. The important question now is whether this holds true in every situation.

DPI insurance limits the amount a person can buy from the insurer. The maximum amounts are $400,000 for a term life plan and $200,000 for a whole life plan.

DPI Term Plan vs Term Plan Through Advisory

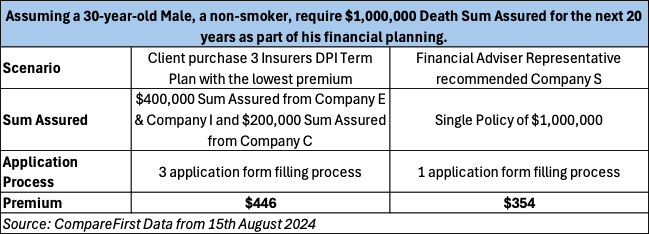

Generally, life insurance plans offer a sizeable discount on large sums assured. To illustrate this, we compared three different life insurance products from three different companies for a hypothetical situation in which an insured needed $1 million in death benefits. We used the same basic parameters—insured is a 30-year-old male, non-smoker—to get the premiums for the three insurance products as low as possible. When you look at the amounts of the premiums, it's clear that you would pay lesser if you purchased a single life insurance policy through an adviser instead of going the route of using a combination of three different insurers with three different insurance products, without mentioning the hassle of going through the application process 3 times with 3 different insurers.

DPI Whole Life Plan vs Whole Life Plan Through Advisory

The DPI Whole Life Plan offers limited options for premium duration—either to age 70 or age 85. Although the premium may be lower compared to a whole life plan obtained via financial advisory, the total premiums paid over the life of the policy will be lower if you choose a Whole Life Plan obtained through advisory services.

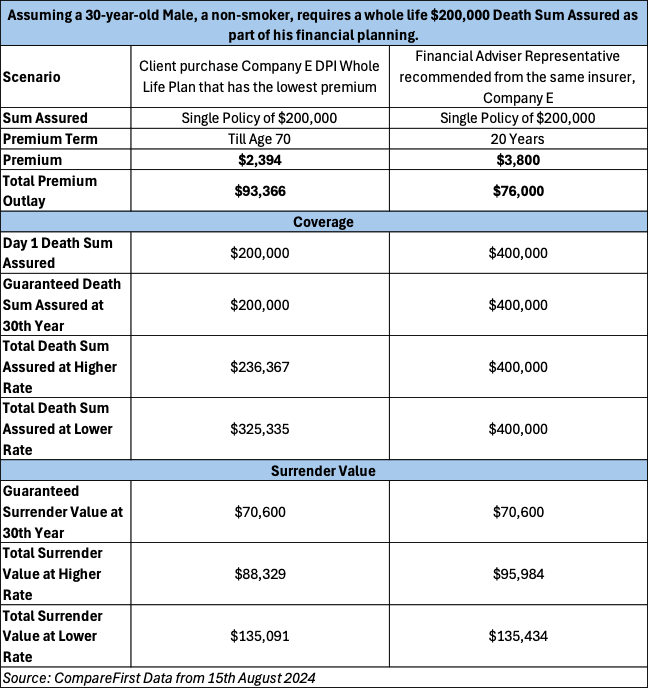

We used the same basic parameters—insured is a 30-year-old male, non-smoker, required $200,000 whole life death coverage, using the same insurer, we had chosen premium till age 70 for the DPI Whole Life Plan and a 20 years premium term for the one through advisory.

While the DPI Whole Life Plan offers only a limited selection of premium payment terms, either to age 70 or age 85, the annual premium for DPI Whole Life plan is lower than the one through advisory. However, the total premium outlay for the whole life plan derived through an advisory relationship is actually lower. Furthermore, the whole life plan attained through an advisory relationship multiplies the death benefit, providing a much greater amount during the years when the insured is economically active. Finally, both life insurance policies—the DPI plan and the plan through an advisory relationship—offer a similar surrender value.

Critical illness insurance plans through advisory tend to cover a more comprehensive set of illnesses and also an option to cover more early-stage critical illnesses. This is really important for people like us, who are in our economically active years, and for the kinds of plans we want.

Whole life plans through advisory can have considerable advantages. This is especially true for the significant death benefit, which can be multiplied in a certain way during the insured's economically active years. A financial adviser can set a whole life plan up to be a lot more flexible when it comes to premium payments, enabling a client to satisfactory financial plan across a period of 5 to 25 years.

Like life insurance, direct purchase general insurance products are available for consumers to buy directly. These include such products as travel insurance, personal accident plans, and home insurance. While the premiums for these products are often indistinguishable from those offered by intermediaries, in the unfortunate event of a claim, the direct-to-consumer model might leave the policyholder somewhat adrift. Intermediaries offer considerable support for navigating the murky claims waters on your own, a benefit that can be hard to fully appreciate if you haven’t experienced it firsthand.

Although direct purchase insurance or online insurance seem convenient, they may not provide the kind of personalised financial planning and coverage one hopes for. Insurance is, of course, a fundamentally serious business. Although it may seem easy and straightforward to buy insurance online, doing so actually requires a good bit of thought and no small amount of understanding. And yet, how many of us would choose, unprompted, to purchase an insurance product one day just for the heck of it? Almost none, I’d wager. Typically, it’s significant life events like buying a car or a house that prompt us to consider insurance. These are what insurers would terms as a “need” to insure. We rarely think about purchasing insurance out of the blue. But when unexpected events happen and we have the right coverage in place, that’s when we truly understand the value of having insurance. It’s often in those moments that we appreciate why we bought it in the first place.

As for our longtime financial health, we almost invariably call on professionals to help us chart that course. And should we need to insure, financial adviser assures us we’re much better off with the kind of coverage that comes via a "plan or strategy" rather than a "direct-to-consumer" purchase. While direct purchase options provide certain conveniences, the inherent value of professional financial advisory cannot be overlooked.

Benefits of Financial Advisers:

In conclusion, while Direct Purchase Insurance offers a straightforward approach to buying life insurance, it may not fulfil all consumer needs as effectively as policies purchased through intermediaries. The expertise of financial advisers proves invaluable in navigating these options and ensuring comprehensive coverage tailored to individual circumstances.

LATEST POST

Articles, events, industry best practices, and news.