Get in touch with our career team!

We are passionate, intelligent and forward-looking team of financial advisers with an eye on the markets and the future.

Published on

LATEST POST

Articles, events, industry best practices, and news.

11 min read

Published on

Financial planning requires insurance. It offers a protective layer between you and the unknown, enabling you to meet your future financial goals even when life throws you curveballs. In Singapore, where the economy has been markedly unstable of late and where lifestyles are changing ever more rapidly, a well-structured insurance plan is your best bet for safe guarding the future you want.

Financial Security: Insurance guarantees that you and your family are safeguarded in the event of an unforeseen occurrence. If something unexpected should happen, like an illness, disability, or death, it ensures that your intimate circle is not weighed down with financial strain.

Peace of Mind: Having insurance can take the edge off the concern that might otherwise accompany the thought of being unable to work or facing overwhelming medical costs. It's a kind of buffer. Some insurance products—investment-linked insurance and whole life insurance, for example—can also serve as means of amassing wealth.

Establishing the appropriate level of life insurance depends on many personal factors, such as the client's income, the size of the family, debts, and future plans. A common approach is to cover 10-15 times the amount of a person's annual income for death and Total Permanent Disability (TPD) and 5 times the amount for Critical Illness (CI). Such advice is easy to follow and gives a decent result when one simply works through the numbers. Yet personalizing the final figure more accurately to an individual's circumstances can yield either a much larger amount or a significantly smaller one.

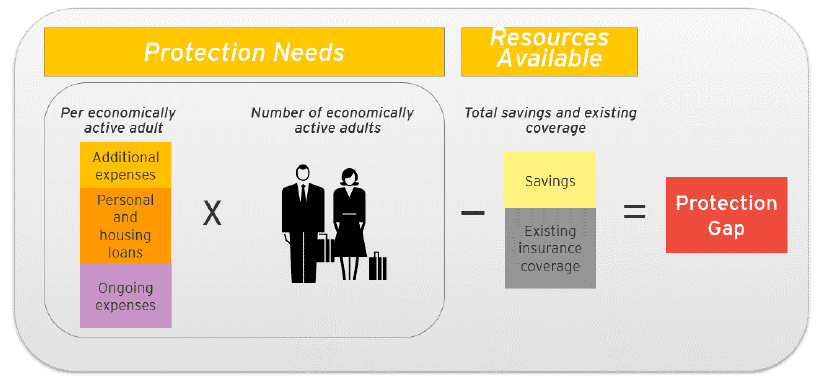

According to the Protection Gap Study Report 2022, the Protection Gap is a metric to estimate the lack of protection against the financial consequences of specific events such as death or CI. Since the approach is not driven by any regulatory requirement worldwide, different methods can be used to estimate the Protection Gap. In this report, the Protection Gap has been calculated as the difference between the Protection Needs (resources required) and the resources available.

Source: Life Insurance Association: 2022 Protection Gap Study – Singapore

Source: Life Insurance Association: 2022 Protection Gap Study – Singapore

The Protection Needs include:

The resources available include:

Normal employees typically enjoy the benefits of employer-sponsored insurance plans, which often encompass group health insurance and a range of other lucrative benefits. Conversely, platform workers & self-employed—like private hire drivers, food delivery workers, financial advisory representatives and real estate agents—have to chart their own course in insurance planning because they work outside of the employer-employee relationship and, therefore, can't access the nice benefits that come along with it.

Normal Employees: While they may depend on the group insurance that their employer provides, they still ought to think about individual plans for further coverage.

Platform Workers & self-employed: Platform workers & self-employed typically lack the benefits that come from having an employer. Because of this, they must take the initiative to find their own insurance. Their focus should be on health insurance, with an eye on the rising costs of medical care; on disability income insurance, to protect against the loss of earnings if a worker is unable to work for a time; and on personal accident insurance, to shield against the kind of happenstance that could strike a worker in any job but that seems particularly risky when one is working without the safety net that an employer provides.

If you have young children or elderly family members, they shape your insurance decisions in a big way.

Young Children: You want to be sure that if the worst should happen, your young children will be taken care of in the same way you are taking care of them now. That means not only life insurance but also health insurance — this is vital as health issues can present significant challenges.

Elderly Family Members: Elderly family members make long-term care insurance essential for families. When you have a family member who is aging, the need for a long-term care policy becomes critical. Products like CareShield Life Supplement or ElderShield Supplement can help relieve some of the financial strain associated with having an elderly relative.

Term Life Insurance

It covers for a set time period. It is usually more affordable and is well suited for those who want basic protection without the kind of serious cash commitment that life insurance often requires.

Whole Life Insurance

Provides coverage for the duration of life and incorporates a cash value element. It can serve as a savings vehicle while extending death benefits.

Health Insurance

It is very important to have health insurance because it protects you from the costs that can arise when you have medical emergencies. For the bulk of the population in Singapore, MediShield Life is the basic health insurance plan that covers them. In addition to what MediShield Life provides, the Integrated Shield Plan gives us health insurance that pays out additional benefits and covers us when we are in private hospitals.

Disability Income Insurance

If you cannot work due to illness or injury, this type of insurance will step in to provide you with income as you recuperate. It is crucial coverage for both employees and platform workers.

Critical Illness Insurance

Provides a one-time payment when you are diagnosed with certain life-threatening diseases, such as cancer or heart disease. The payment is intended to help defray the cost of treatment and to replace the income that you and your family would lose while you attempt to get well and return to work.

Personal Accident Insurance

Protects against injuries or deaths that happen by chance. This is especially pertinent for platform workers especially private hirers and food delivery workers, who have a heightened risk of getting hurt while they work.

Universal Life Insurance

This product packages life insurance with an investment component that can increase in value over time. It provides policyholders with several depths of coverage and a variety of premium payment and death benefit options that allow them to tailor the policy to their needs.

Long-Term Care Insurance

CareShield Life Supplement and ElderShield Supplement are products that help if the individual requires long-term care. If a family member has to pay out of pocket, it could lead to an enormous dent in their savings. These plans help bridge that gap.

Investment-Linked Insurance

These policies provide two kinds of benefits—insurance and investment. They are designed to pay death benefits, like a traditional life insurance policy, but they also may help accumulate cash value, unlike most traditional policies. The expected returns on these policies can be higher than on typical whole life policies, but that also means they can carry a bit more risk. It is important to note that such products may not be suitable for whole life protection purposes.

Hospital Income Insurance

The plans that pay cash in the event of a person's hospitalisation are called hospital income plans. For platform workers & self-employed, having an income plan during hospitalisation is particularly valuable. Platform workers & self-employed typically do not have a steady income, so when they are unable to work for any reason—particularly if they are recovering from a serious medical issue—their lack of a payday can make their life very difficult. Platform workers & self-employed can’t always rely on family or friends for support, and they usually do not have a recovery fund. Having an income plan that offers cash benefits for days spent in the hospital can go a long way towards covering the costs that are associated with being sick and towards allowing a person to focus on recovery.

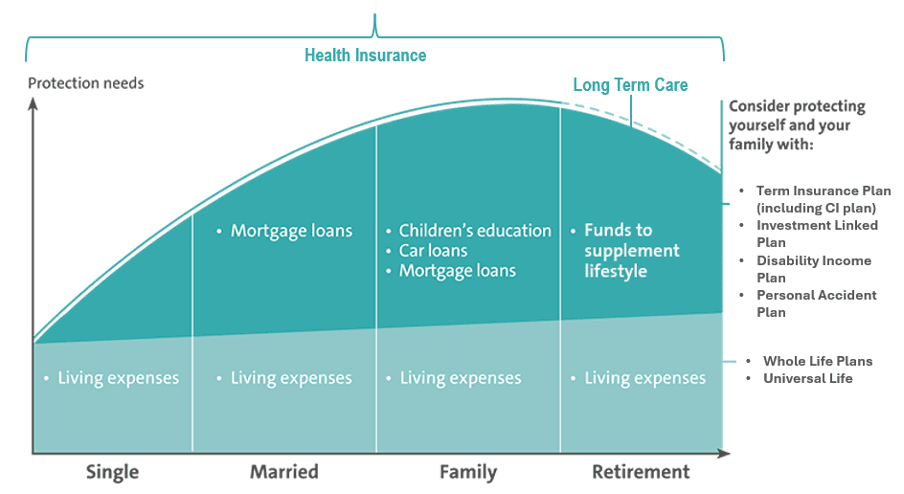

The accompanying graph may be used as a guideline for arranging your various life insurance policies based on the different stages of your life.

Although the employer-provided group insurance may seem sufficient, you should not base your insurance planning solely on it. Group plans often come with a bunch of limitations and might not cover all personal circumstances or conditions adequately. Individual plans can and do cover these types of conditions and circumstances, and they also might align better in terms of financial objectives, with the solutions you choose for your family.

The 2022 Protection Gap Study for Singapore has brought to light an alarming problem: the significant lack of protection available to platform workers in the country. While there are many protection gaps among the overall population in Singapore, the study found that, if anything, these gaps are even more dire for platform workers. Likely due to the nature of how they work, platform workers tend to need a lot more coverage and protection in case of certain events, such as death or serious illness, than the overall population does. The estimated value for platform workers death coverage (i.e., life insurance) is about S$55 billion, with a staggering gap of 59% (S$32 billion) uncovered. For serious illness (i.e., CI) coverage, 91% of needs are not met, with a coverage gap of about S$20 billion.

The larger protection gaps for platform workers are caused by the lower savings (in CPFs and other accounts) and lower insurance coverage of platform workers compared to the average adult in the Economically Active (“EA”). Many platform workers, particularly those in the lowest income quintile, do not have the wherewithal to protect themselves and their families financially. An additional survey of EAs shed more light on the issue. It discovered that, like the EA population, the top three worries for platform workers are centred on health concerns, ageing, and being unable to work because of a serious condition.

A much larger slice of platform workers (33%) pointed to job/income instability as a prime concern stemming from the inherently unstable nature of platform work, compared to just 23% of EA adults. Moreover, the survey showed that more than 60% of platform workers either do not have access to group coverage or do not know if they have group coverage. This lack of protection is pathway No. 1 to a huge gap in platform workers' insurance coverage. Closing that gap is going to take several different efforts, a multi-pronged approach.

Insurance companies have to increase their efforts to create products that this segment can access and afford. Their efforts should be coupled with those of at least one other player in the protection sector—policymakers—who can enhance the social safety net for platform workers. The need is clear: According to MOM's latest labour force report released in January, there were more than 88,000 platform workers in 2023 and this number exclude all the self-employed professionals such as financial adviser representatives and real estate agents. These workers are self-employed and use online platforms to match themselves to delivery and transport jobs. And platform workers & self-employed will continue to proliferate in our economy going forward.

The challenges have been laid bare by the 2022 Protection Gap Study, and now it is up to all interested parties to work in cooperation to close the serious gaps that have been exposed.

In Singapore, financial planning is incomplete without insurance. Understanding various insurance products and their significance based on individual situations—whether one is an employee, a platform worker, or self-employed—enables necessary and wise decisions that help secure a family’s future, especially when young children or elderly family members are part of the household. Making the necessary decisions and securing comprehensive personal insurance provides a means of survival when unpredictable events takes place.

LATEST POST

Articles, events, industry best practices, and news.