Get in touch with our career team!

We are passionate, intelligent and forward-looking team of financial advisers with an eye on the markets and the future.

Published on

LATEST POST

Articles, events, industry best practices, and news.

10 min read

Published on

The evolution of healthcare financing in Singapore has been substantial over the years. MediShield Life, together with the Integrated Shield Plans, provides essential medical coverage to the citizens. Nevertheless, in light of recent trends and concerns regarding the inflation of medical costs, important discussions have been sparked about the sustainability of these plans and the behaviour of the policyholders.

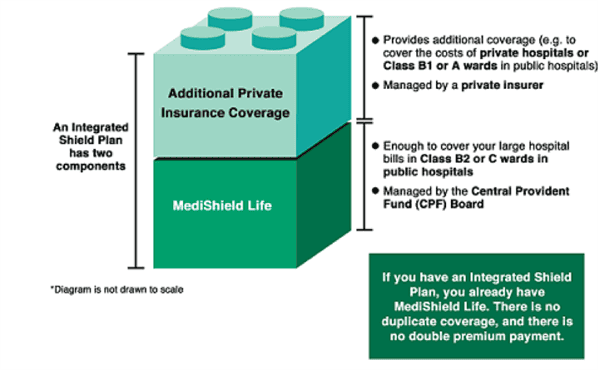

The fundamental health insurance program set up by Ministry of Health (MOH) that is compulsory to all Singaporeans and Permanent Residents (PR) is called MediShield Life. This basic insurance plan covers a substantial amount of the health care costs incurred by Singaporean and PR in a subsidised ward in a Government Hospital or Restructured Hospital. Although it is a co-payment plan, meaning that the user is financially responsible for a certain portion of his or her medical costs and surgical procedure are covered at up to a limit according to the surgical table after the deductible has been met, even with the deductible and co-payment figured in, a person in MediShield Life pays less than he or she would pay in the absence of such a plan. The plan is designed to ensure that all Singaporean and PR can access necessary medical services in Government Hospital or Restructured Hospital.

Integrated Shield Plans (IPs) are additional private insurance products that complement MediShield Life which is entirely optional. These plans offer enhanced coverage for hospitalisations, allowing policyholders to enjoy greater benefits such as private room accommodations and coverage for outpatient treatments and even private hospitals. While these plans provide valuable enhancements, they also raise concerns regarding the over-utilisation of healthcare services. Key features of Integrated Shield Plans include:

Riders can be attached to the integrated shield plans of policyholders. Adding riders can make the plans better, the riders are payable using cash, you can’t use your CPF MediSave to pay the premium. The added-on riders can make the policy provide what it wasn't originally set up to provide. The plans, with riders, can give additional financial protection. And they can extend the reach of the original base policies by reaching into areas not covered by the base policies.

Some of the riders pay the deductible amount between the policyholder and the insurance company. They lessen the out-of-pocket expenses the policyholder has during hospitalisation in a covered event. The riders do not eliminate the co-insurance part of the payment, but they help the policyholder pay a reduced amount. Higher co-insurance amounts can certainly be a financial burden. If you have a rider, it will help you in this situation.

Some insurers offer riders that specifically increase the claim limits for medications included in the cancer drug list. These riders are particularly valuable for patients undergoing extensive cancer treatment, as they can significantly reduce the financial strain associated with costly medications.

Source: MOH Website

Source: MOH Website

According to the then Senior Minister of State for Health, Chee Hong Tat, in 2018, the zero co-payment feature of full riders on integrated shield plans resulted in a “Buffet” Mindset, leading to over-consumption, over-servicing and over-charging of healthcare services.

For those who see things from an economist's point of view, the buffet metaphor seems to make initial sense. It is implicit in Integrated Shield Plans that have zero co-payment coverage and lead to overconsumption, and that is a well-known moral hazard in the insurance market.

An optional insurance plan usually draws in people who think they are going to need a lot of benefits. This is a well-known problem in insurance. It is called adverse selection.

Insurers face rising costs because of both happenings. They then pass those rising costs on to consumers so that they can remain in the business of insuring.

The current insurance landscape presents a pressing concern. It gives way to the notion, among insured patients, that they are given a "buffet" of services from which to choose. Not only are most services covered by insurance, but even the insured patient today pays so little that he or she is largely unconcerned about the amount being spent. On this pay-as-you-go basis, health insurance seems more like a scholarship program.

An increasing number of people are choosing Integrated Shield Plans. Now there's a worry that these may inflate future medical costs. Of course, this is the opposite of what health insurance is supposed to achieve. But why might these plans lead to inflation? One reason could be that insured patients use more medical services. And part of the reason they use more services is because they can and because they believe they should.

In addition, certain private specialists might exploit the insurance system, operating on patients or ordering tests that are not truly necessary. This practice of performing unnecessary work can inflate medical costs, to the detriment of patients and the insurance system as a whole.

MOH has taken action recently against six doctors who did not comply with the regulations for making claims under the MediShield Life insurance program. Of those six, two were singled out for particularly severe treatment: their MediSave and MediShield Life accreditation have been suspended for six months, so patients receiving treatment from these providers during this time will be unable to use MediSave or MediShield Life to cover the costs. The MOH has taken these doctors and their offices to task in a serious way in order to uphold the basic integrity of the systems of billing and insurance that are essential to the operation of any healthcare system, including Singapore's. The improper claims, in this case, were the "overcharging" of patients and the misrepresentation of services provided to patients.

In an attempt to overcome these difficulties, some insurance companies are putting into place certain measures. Among these are "no-claim" discounts and "claim experience" based premiums, which are used to figure out how much to charge policyholders.

No-Claim Discounts

Discounts on premiums upon renewal may be offered by insurers to entice even more people to purchase policies. The reason for these discounts is always the same: not making claims means the insured is using the policy as intended, which is practically and, some might say, morally, a good reason to give a no-claims discount.

Claim Experience-Based Premiums

Some Insurance companies have used this system to compute premiums. It considers the number of claims a policyholder has made over the previous policy year. The more claims, the higher the premiums at renewal time. The fewer claims, the lower the premiums. Insurers hope this will create a strong, direct correlation (and in the minds of their policyholders, a causative one) between the policyholder’s behaviours—making claims or not—and the cost of the policy.

Insurers aim to prevent service overuse while maintaining proper coverage for those requiring it by charging premiums that reflect the true level of risk an insured party represents.

In 2023, MOH made some big waves in the country's health care sector. It introduced amendments to the health insurance framework, particularly the integrated shield plan, which serves as a medical insurance supplement for Singaporeans. These changes were not minor. They could well be characterized as significant. They could also be said to have a clear target: cancer.

The Life Insurance Association (LIA) declared that integrated shield plans would stay as they are for the next two years. This means that any premium increases will be put off until September 2024, when a scheduled review will happen.

As we near that important time, we must look closely at the current environment, which can be summed up in two words: "high" and "rising." Medical insurance claims are coming in at high rates, and inflation in the healthcare sector is bad, too. And no matter what happens next, this situation is bound to have some effect on policyholders.

Several things could happen as we head toward the September 2024 premium review.

Singapore's healthcare financing system relies fundamentally on two components: MediShield Life and Integrated Shield Plans. Both pay for "reasonable and necessary" medical expenses incurred when those enrolled pay for hospitalisation and surgery. But with medical inflation running at 10 percent a year, and with potential malfeasance by providers in over-utilisation and by payers in under-utilisation, it is vital that both insurers and insured behave responsibly. Otherwise, this very "sustainable" system becomes contradictory and a danger to future generations.

LATEST POST

Articles, events, industry best practices, and news.